Forty years ago, US Federal Reserve Chairman Paul Volcker stopped inflation with radical and painful interest rate hikes. It was either that or enduring more inflation-induced suffering. So are we facing a similar scenario today?

“What we are seeing now is clearly stagflation,” Professor Hans-Werner Sinn explained at a congress at the beginning of April 2022. According to Sinn, inflation rates have not yet peaked, and the economy is facing difficulties as a result of supply shocks. This despite the fact that many Western economies experienced strong growth after the initial Coronavirus shock.

For example, for US companies, 2021 was the most profitable year since 1950, and they benefited from huge stimulus packages, full order books and a booming labor market. At the same time, however, prices were increasing – something that was thought to be temporary. But since then, the environment has changed noticeably.

What is stagflation?

The term stagflation is a combination of the words stagnation and inflation. It describes a situation in which three trends come together:

a high inflation rate

a slowing economic growth rate

high or rising unemployment

The term was first used in 1965 by the British politician Iain Macleod in a speech to Parliament. At the time, both high inflation and high unemployment prevailed. Macleod described the situation as follows: “We now have the worst of both worlds – not just inflation on the one side or stagnation on the other, but both of them together. We have a sort of ‘stagflation’ situation.”

This kind of scenario has dramatic consequences for large segments of the economy and cannot be overcome without making painful adjustments. The dilemma is that measures to lower inflation, such as interest rate hikes, can initially put a further drag on growth and aggravate unemployment. In addition, if companies do not get the funds they need due to supply bottlenecks, for example, production can decline even though demand exists and order books are full.

The wage price spiral

In the 1960s, the combination of high inflation rates and high unemployment was inconceivable to many economists. It was assumed that high unemployment would be accompanied by low price increases – and vice versa.

But in the 1970s, it became apparent that as soon as employees and companies expect inflation to further increase, this theory no longer holds true. A wage price spiral emerged: persistent price increases were factored into wage negotiations, and wages – and thus companies’ costs – rose faster and faster, further fueling inflation.

In the late 1960s, inflation rates in the US were rising as a result of expansionary monetary policy. This was intended to improve the situation in the labor market. At the same time, national debt had also grown significantly, as a result of the Vietnam War.

In addition to this came the failure of the Bretton Woods system in 1971, when the US stopped the US dollar’s convertibility to gold. The US dollar became freely tradable and depreciated more and more. From 1971 to 1978, it lost around 30 percent, which drove up the price of commodities and precious metals such as gold.

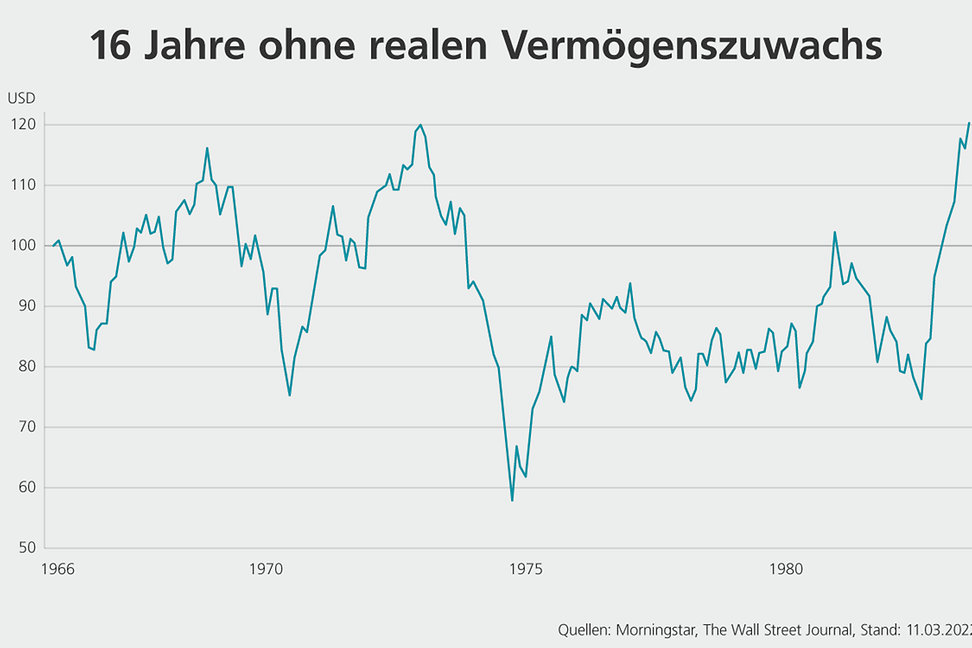

Von 1966 bis 1982 erzielten Anleger mit grossen US-Blue-Chip-Aktien unter Einbezug reinvestierter Dividenden und nach Bereinigung um die Inflation eine Nullrendite. Per 1974 hatten sie real betrachtet fast die Hälfte ihres Werts verloren.

This trend was further fueled by the oil crisis that emerged following OPEC’s decision to cut production in 1973 for political reasons. From just over 3 US dollars in 1972, the price rose to a peak of 15 US dollars by 1975. This led to higher inflation and weaker growth, even recession, in many industrialized countries, marking the beginning of stagflation.

In parallel to this came a collapse in stock prices in 1973 and 1974. After a period of calm, a second oil crisis followed in 1979 due to reduced production as a result of the turmoil in Iran. This was the last straw, and in the US, inflation once again reached the double digits seen in 1974/1975, rising to 14.8 percent in March 1980.

The causes of stagflation

One explanation for the existence of both stagnation and inflation is that the economy is facing a supply shock. This can happen when the price of oil rises rapidly. As a result, other prices rise and production becomes more expensive and less profitable – and ultimately economic growth slows. At the turn of the millennium, a study of stagflation in the 1970s provided evidence of this relationship.

But stagflation can happen even in the absence of supply shocks. According to studies, the persistent price increases for industrial goods that took place before the oil price hike in 1973/1974 were largely the result of the prevailing monetary policy. The sharp rise in oil prices in the 1970s is therefore now considered not a cause, but an accelerator of stagflation.

The emergency brake

The role of monetary policy in fighting inflation was underestimated for a long time. However, its importance became clear at the latest in August 1979, when Paul Volcker was appointed the new head of the US Federal Reserve. He resorted to radical measures and raised interest rates to as much as 20 percent. In doing so, inflation was brought under control again in the span of two years.

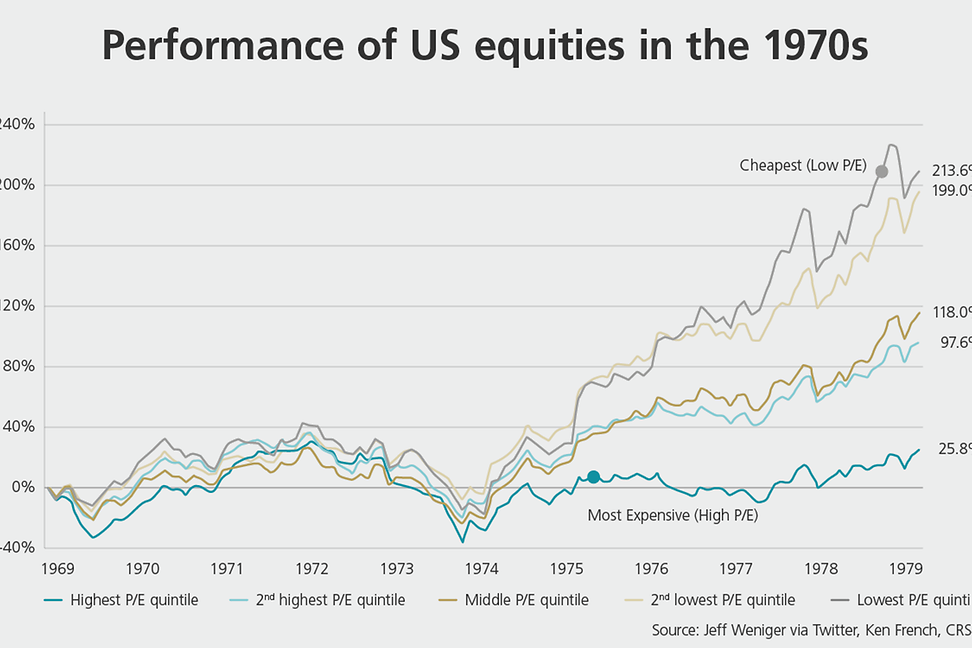

During the 1970s, when inflation rates were very high, the 20 percent of stocks with the lowest valuation – as measured by price-to-earnings ratios – performed significantly better than the highest-valued stocks.

However, the interest rate hikes were also very painful. The US economy slid into a recession and unemployment rose. So in the short term, things got worse before they got better. The US dollar subsequently became very strong for several years, and commodity prices fell (finally).

The negative consequences of this unexpectedly radical approach also spread to other countries. They are considered a contributing factor to the so-called “lost decade” in Latin America. By 1983, the hurdles had been overcome and growth picked up again. By the fall of 1982, the stock market had risen again – this upswing lasted a full 18 years.

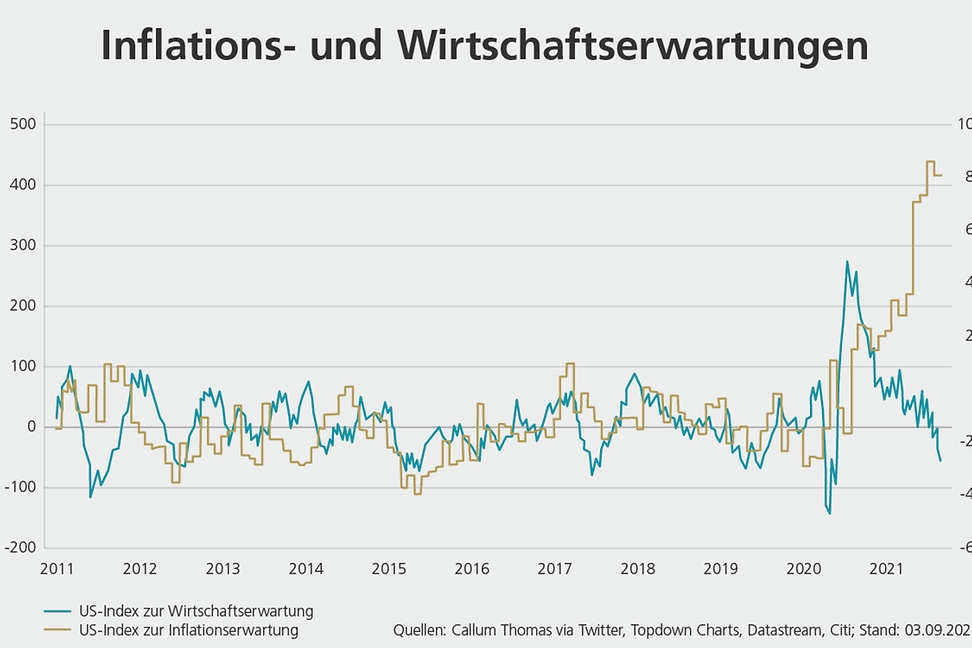

High inflation expectations, low economic expectations: In the fall of 2021, there were increasing signs that another period of stagflation could lie ahead.

Another round of stagflation ahead?

After four decades of decreasing inflation rates, prices in March in the US [insert link] had suddenly increased by 8.5 percent – the same levels reached in 1981. This trend is also clearly taking place in Europe, as indicated by the big jump in producer prices.

According to Professor Sinn, prices there have increased significantly year on year (France 22 percent, Austria 24 percent, Spain 36 percent, Italy 42 percent). By comparison, at the time of the oil price shock in the 1970s, prices in Germany had “only” increased 15 percent.

Market information from our research experts

How we see the markets

LGT’s experts are always busy analysing global economic and market trends. Our research publications on the international financial markets, sectors and companies will help you make informed investment decisions.

Some experts are drawing parallels between the war in Ukraine and the first oil crisis in 1973, seeing both as accelerators for inflationary tendencies. According to the controversial economist Nouriel Roubini, the current stagflationary environment actually emerged during the pandemic. In addition to the disruptions in global supply chains due to Coronavirus, the global economy has suffered a second negative shock on the supply side with the war in Ukraine, which is further exacerbating the situation.

Tight supply and high commodity prices are combining with the effects of loose monetary and fiscal policy – as well as a weaker economy. Central banks are thus facing the same dilemma as Paul Volcker did: they should normalize monetary policy quickly in order to establish and prevent wage-price spirals. But it could be difficult to proceed radically enough without triggering a severe recession and a crash in financial markets. It remains to be seen how the scenario will play out this time around.

Related

Investment strategy

Health and well-being: An opportunity for investors

"Who wants to live forever?" Eternal life may not yet be within our reach, but for more and more people, a longer life certainly is.

Considerable progress has been made in recent decades with regard to medical treatment options and technologies. In addition, more and more sick people around...

Investment strategy

How to profit from falling share prices

If you think share prices are set to drop, you don’t have to lie down and take the pain. Instead, you can profit from any fall using a process called short selling.