- Home

-

Private banking

-

LGT career

Central banks like the Federal Reserve do not use one specific monetary policy theory to determine their key rate - they apply several different approaches; one of these is the Taylor rule.

The Taylor rule is a straightforward approach used to analyze and describe monetary policy, and is therefore very popular. However, its relevance should not be overestimated.

The responsibilities of central banks include responding appropriately to the economic environment and achieving certain outcomes - such as price stability - for the domestic economy. One tool for assessing the economic situation is the Taylor rule, which was developed in the 1990s by US economist John B. Taylor.

This formula calculates the optimal level of a central bank's key rate and focuses on two main factors: an economy's current price level and its production output. If the overall economy's potential output is not being fully exploited or if inflation is below the target level, the key rate should be lowered to below the equilibrium rate (an interest rate that is consistent with sustainable productivity growth with full employment and stable inflation over the long term) - if the inflation rate is above target and potential output is too high, the key interest rate should be increased.

The financial crisis is a good example of how the Taylor rule works in practice. In 2008, potential output and inflation plummeted. To stimulate economic growth, central banks around the world lowered interest rates.

While reacting to the crisis quickly by lowering interest rates was undisputedly the correct thing to do, the reluctance to raise interest rates in recent years is astonishing. The Bank for International Settlements has long criticized this asymmetrical behavior of central banks. It faults them for reacting to every small shock by lowering interest rates without subsequently sufficiently raising them again.

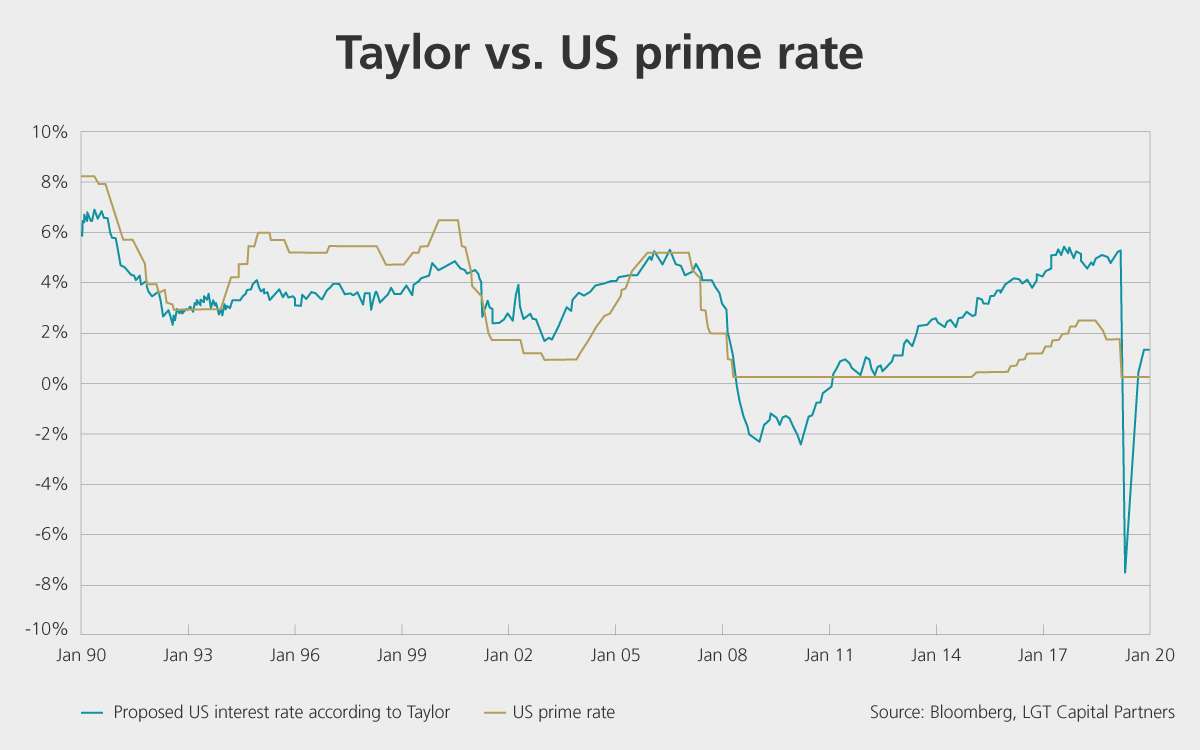

John B. Taylor is also critical in this regard. He says that instead of leaving the federal funds rate at a low level, the Federal Reserve should have increased it sooner and more gradually. A comparison of the US key rate and the US interest rate using the Taylor rule confirms these statements. The discrepancy between these two figures has been very high over the past few years:

The question arises as to whether the Taylor rule is an appropriate guide for setting interest rates. This is because in practice, central banks only apply it unilaterally when lowering interest rates. One of the challenges when applying this monetary policy rule lies in the weighting of input variables.

If the central bank's primary objective is to combat inflation, it will place greater emphasis on the "price level" variable and less on "output". The weightings must thus be estimated individually by each central bank according to its mandate. However, difficulties arise not only when determining the weightings, but also when estimating the variables.

For example, the deviation of GDP (gross domestic product) from "potential output" is difficult to determine. In addition, the unused capacity of part-time employees is often not included in statistics, which results in true potential output being underestimated. Further to this, numerous challenges also exist in determining the price level. These limitations in both the measurement of variables and weighting put the relevance of the Taylor rule into perspective.

The increasing criticism of central banks is understandable. The persistently extremely low interest rates create a dangerous incentive for further lending, which has negative effects on financial market stability. The low interest rates of recent years have increasingly driven investors into risky asset classes. If the economic outlook improves again once the Covid-19 crisis has been overcome, calls for tighter monetary policy will become louder again.

However, relying on the Taylor rule to this end is unjustified. When determining the optimal level of the key rate, the Taylor rule serves merely as a point of reference that cannot in itself explain the complex key rate models used by central bankers. For central banks to apply only the Taylor rule would be a mistake - with consequences for the entire economy.

Andreas Vetsch is a research analyst at LGT Capital Partners and in this role, also monitors the monetary policy of central banks.

He and his colleagues in Asset Management look for attractive investment opportunities and identify the best portfolio managers. They also manage a substantial portion of the assets of LGT’s owner, the Princely House of Liechtenstein.